The end of summer and the start of the school year always seem to be a catalyst for conversations about college savings and where they fit into larger, long-term financial strategies. In particular, the 529 college savings plan, with its nuanced tax advantages, can be cause for confusion.

No matter how young your children or grandchildren are, it’s never too early to start thinking about saving for their education. Even relatives can help contribute to a child’s 529. Let’s take a look at the benefits and (potential drawbacks) of a 529 plan.

Why a 529 plan is worth considering:

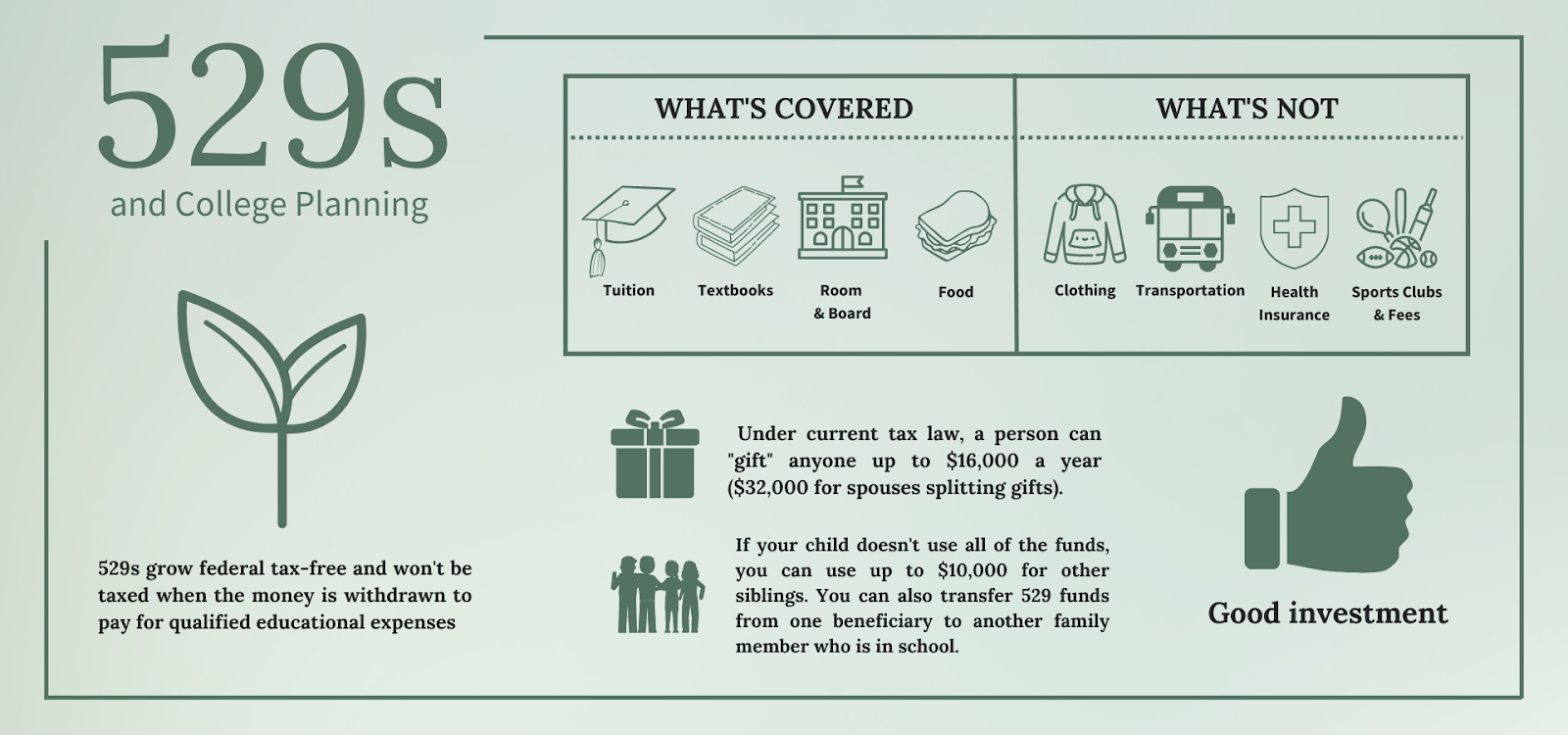

- How to fund a 529 plan is a big consideration for many people. But did you know that you could open an account with a gift? Under current tax law, a person can "gift" anyone up to $16,000 a year ($32,000 for spouses splitting gifts). The recipient typically owes no taxes and doesn't have to report the gift as income. That means you can make relatively large annual contributions without worrying about the gift tax.

- You can also make larger contributions, up to $80,000 ($160,000 for married couples, filing jointly), and still avoid the gift tax by treating the contribution as though it were made over a five-year period.

- Even though a contribution to a 529 plan leaves your estate, it still remains in your control, since you oversee all of the account’s investment choices, beneficiary designations, and distributions.

- Earnings in a 529 plan grow federal tax-free, and won’t be taxed when the money is withdrawn to pay for qualified educational expenses, such as tuition, fees, books, supplies, and computers.

- Another great benefit to know about - if your child doesn't use all of the funds, you can use up to $10,000 for other siblings. You can also transfer 529 funds from one beneficiary to another family member who is in school.

Using a 529 plan for college savings comes with a host of benefits, but there are some other factors to keep in mind as well. Money in a 529 plan can only be used for education. If your designated beneficiary decides not to go to college, you can always transfer the plan to another beneficiary. You can also withdraw money from a 529 plan for reasons besides education but at a 10% penalty and the money will also be subject to income taxes.Remember, we said this money was given as a gift. It gets taxed if it's withdrawn early.

Whether or not you decide a 529 plan is right for your long-term financial goals, starting to save for college is a great way to open up the discussion around your estate with your children and grandchildren. If you have questions about 529s and whether or not they are a fit for you, feel free to reach out to our team.